Debtproof 😎

A simple rule to keep loans under control

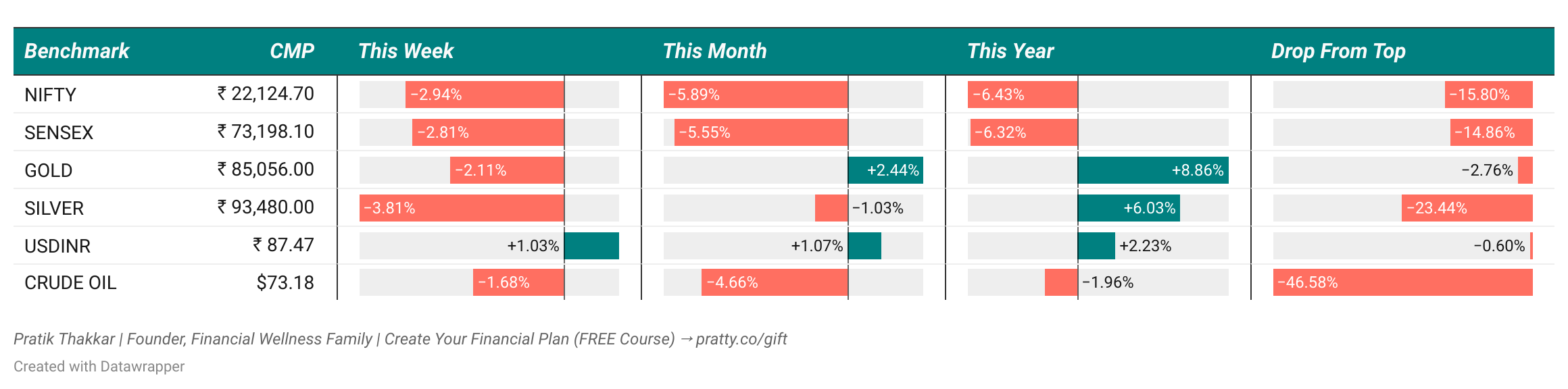

📊Weekly Market Snapshot

It was a brutal week for the markets - Nifty couldn’t catch a break, slipping for the fifth straight month, its worst stretch in nearly 30 years.

Global jitters, FII outflows, and tariff worries kept investors on edge.

IT stocks took the biggest hit, while even defensive sectors struggled to stay afloat.

With GDP data now in, all eyes are on whether this downturn finds a floor or keeps sliding.

Buckle up - March could be just as bumpy.

💡Weekly Family Financial Wisdom

How Much Debt Is Too Much? The 28/36 Rule Has the Answer

Debt can become a burden when it takes away peace of mind. The 28/36 rule helps families in India know how much is safe to borrow.

1. What the 28/36 Rule Means

The 28/36 rule says that housing costs should not be more than 28% of gross monthly income, and total debt payments should not go over 36%.

For example, if a family earns ₹1,00,000 per month, housing expenses should stay below ₹28,000, and all loan EMIs combined should not cross ₹36,000.

Following this rule keeps financial stress away.

2. Why Home Loan Lenders Use It

Banks and NBFCs use the 28/36 rule to check if a borrower can afford a loan.

If a home loan EMI goes beyond the 28% limit, the bank might reject the application or ask for a bigger down payment.

Knowing this rule helps buyers plan before applying for a loan.

3. Helps Avoid Debt Traps

Too much debt can lead to missed EMIs, high interest, and credit score damage.

If a person spends more than 36% of income on loans, an emergency like a medical bill can cause financial trouble.

Keeping debt under control ensures peace of mind.

4. Supports Smart Financial Planning

Following the 28/36 rule makes it easier to save for future goals.

Families who manage debt well can afford education, vacations, and retirement without worry.

Sticking to this rule brings long-term financial security.

Financial wellness comes from smart decisions. The 28/36 rule is a simple way to stay in control of money and build a stress-free future.

🛠️ Question of the Week

⚠️Disclaimer

This newsletter is for educational purposes only and should not be construed as investment advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

Did you find this newsletter helpful?

Share it with another family who might benefit: